If you’ve ever started researching buying a house and found yourself drowning in financial jargon, you’re not alone. Two terms that trip people up constantly are “home loan” and “mortgage.” You hear them used interchangeably all the time — by real estate agents, lenders, even your neighbors who just bought a place last spring. But are they actually the same thing? And does the distinction even matter when you’re trying to buy a house?

Short answer: they’re closely related, but not identical. Understanding the difference can help you ask better questions, read your documents more confidently, and ultimately feel less lost in what’s one of the biggest financial decisions of your life.

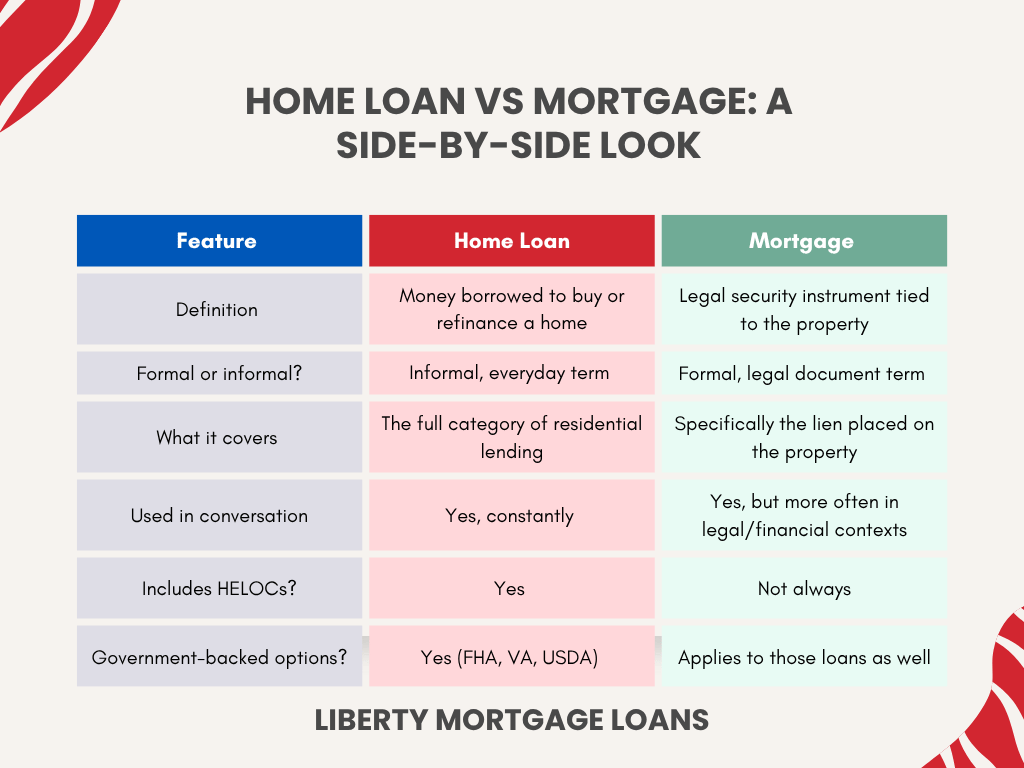

What Is a Home Loan?

A home loan is exactly what it sounds like — money you borrow to purchase or refinance a home. It’s the broader, more informal term that most people use in everyday conversation. When someone says “I’m getting a home loan,” they mean they’re borrowing funds from a lender (a bank, credit union, or mortgage company) to buy residential property.

The term “home loan” is really more of a category than a specific financial product. It covers a wide range of borrowing options, including:

- Conventional loans

- FHA loans

- VA loans

- USDA loans

- Jumbo loans

- Home equity loans

- Home equity lines of credit (HELOCs)

Each of these is a type of home loan with its own rules, rates, and eligibility requirements. Some are backed by the federal government; others aren’t. Some are designed for first-time buyers; others are built for veterans or people buying in rural areas.

So when you walk into a lender’s office and say you need a home loan, you’re starting a conversation — not completing one.

What Is a Mortgage?

Here’s where it gets a little more technical. A mortgage isn’t actually the loan itself. Technically speaking, a mortgage is a legal agreement — a security instrument — that ties your home to the debt you owe. It’s the document that gives the lender the right to take your property through foreclosure if you stop making payments.

In practical terms, though, most people (including most lenders) use “mortgage” to refer to the whole package: the loan plus the legal agreement attached to it. When you close on a home purchase, you sign a promissory note (which is the actual loan agreement) and a mortgage or deed of trust (which is the security instrument). Together, these two documents create what everyone just calls your “mortgage.”

The distinction matters most in legal and real estate contexts. If you’re talking to a title company, a real estate attorney, or reading a deed of trust, the word “mortgage” has a precise technical meaning. In casual conversation? It’s basically synonymous with home loan.

Home Loan vs Mortgage: A Side-by-Side Look

Looking at them this way, you can see why people mix them up. In daily life, the difference rarely comes up. But when you’re signing paperwork, you’ll want to know what each document actually means.

Why Do People Use the Terms Interchangeably?

The financial industry has done a pretty good job of blurring this line for decades. Lenders advertise “mortgage rates” when they mean the interest rate on a home loan. News outlets report on “mortgage applications” when they’re tracking how many people are borrowing to buy homes. Even the government’s Consumer Financial Protection Bureau often uses both terms in the same sentence.

The overlap happens because, in the vast majority of U.S. home purchases, you get both at the same time. You take out a home loan and sign a mortgage document simultaneously. They’re bundled together so consistently that separating them feels academic.

That said, there are situations where the two diverge. A home equity loan, for example, is a type of home loan — but in some states, the security instrument used is a “deed of trust,” not a traditional mortgage. Technically, you have a loan without a mortgage. Confusing? Yes. But the lender still has a lien on your property, so the practical effect is the same.

The Types of Home Loans You Should Actually Know

Since “home loan” is the broader umbrella, it’s worth knowing what’s under it. Here’s a breakdown of the main loan types you’ll encounter in the U.S. market.

Conventional Loans

These aren’t backed by any government agency. They typically require a higher credit score (usually 620 or above) and a down payment of at least 3% to 5%. If you put down less than 20%, you’ll pay private mortgage insurance (PMI) until you build enough equity.

FHA Loans

Backed by the Federal Housing Administration, FHA loans are popular with first-time buyers because they allow down payments as low as 3.5% and accept credit scores starting around 580. The trade-off is mortgage insurance premiums, which stay on the loan for its entire life in most cases.

VA Loans

Available to eligible veterans, active-duty service members, and surviving spouses, VA loans are backed by the Department of Veterans Affairs. No down payment required, no PMI, and competitive interest rates. One of the best loan products available — if you qualify.

USDA Loans

Backed by the U.S. Department of Agriculture, USDA loans are designed for buyers in eligible rural and suburban areas. They also offer zero down payment options and low mortgage insurance costs.

Jumbo Loans

When the loan amount exceeds the conforming loan limits set by Fannie Mae and Freddie Mac (currently $726,200 in most U.S. counties for 2024), you’re in jumbo territory. These loans carry stricter requirements and usually need larger down payments and higher credit scores.

Home Equity Loans and HELOCs

These use the equity you’ve already built in your home as collateral. A home equity loan gives you a lump sum with a fixed rate. A HELOC works more like a credit card — a revolving line of credit you can draw from as needed. Both are types of home loans, but they’re not mortgages used to purchase a property.

How Interest Rates Work on Home Loans

Your interest rate is one of the most important numbers in the entire home-buying process. Even a half-point difference in your rate can mean tens of thousands of dollars over the life of the loan.

Rates come in two main forms:

Fixed-rate loans lock your interest rate in for the entire loan term — typically 15 or 30 years. Your monthly principal and interest payment stays the same from month one to month 360. Predictable, stable, easy to budget around.

Adjustable-rate mortgages (ARMs) start with a lower fixed rate for an initial period (say, 5 or 7 years), then adjust periodically based on a market index. You might save money early on, but your payment can rise after the adjustment period kicks in. ARMs work well if you plan to sell or refinance before the rate adjusts.

Lenders determine your specific rate based on several factors: your credit score, debt-to-income ratio, loan-to-value ratio, the type of loan, and broader economic conditions like the federal funds rate.

“Even a 0.5% difference in your mortgage rate on a $400,000 loan can cost or save you over $40,000 across a 30-year term. Rate shopping isn’t optional — it’s essential.”

The Mortgage Process: What Happens from Application to Closing

Understanding the basic flow of getting a mortgage helps reduce anxiety. Here’s how the process typically moves:

- Check your credit and finances. Know your credit score, calculate your debt-to-income ratio, and figure out how much you can realistically put toward a down payment.

- Get pre-approved. A lender reviews your financial documents and gives you a pre-approval letter stating how much they’re willing to lend. This is different from pre-qualification, which is a softer, less verified estimate.

- Shop for homes within your budget. Your pre-approval amount isn’t your target — it’s your ceiling.

- Submit a formal loan application. Once you’re under contract on a home, you formally apply for the mortgage.

- Underwriting. The lender’s underwriter verifies everything — your income, assets, employment, the home’s appraisal value. This is where deals can slow down or fall apart.

- Clear to close. Once underwriting is satisfied, you get the green light to close.

- Closing day. You sign a stack of documents (including that mortgage instrument), pay closing costs, and get the keys.

The whole process typically takes 30 to 60 days from application to close, though it can move faster or slower depending on the lender and your situation.

Common Mistakes People Make When Confusing These Terms

Mixing up home loans and mortgages is mostly harmless in conversation. But in a few situations, the confusion can actually cost you.

Mistake #1: Assuming all home loans require a mortgage.

Some loan types use a deed of trust instead. In states like California, Texas, and Virginia, deeds of trust are far more common than traditional mortgages. The practical difference is in the foreclosure process — deeds of trust typically allow for non-judicial foreclosure, which is faster.

Mistake #2: Thinking a home equity loan is the same as a cash-out refinance.

Both let you access your home’s equity, but they work differently. A cash-out refinance replaces your existing mortgage with a new, larger one. A home equity loan is a second, separate loan. The right choice depends on your current rate and how much equity you want to tap.

Mistake #3: Focusing only on the interest rate.

Your APR (annual percentage rate) includes the interest rate plus fees — origination fees, points, and other lender costs. Two lenders quoting the same interest rate can have very different APRs. Always compare APRs when shopping loans.

Does the Difference Actually Matter for Your Home Purchase?

For most buyers? Not day-to-day. You’ll hear both terms constantly throughout the process, and in context, it’s always clear what’s being discussed. Your lender will explain each document before you sign it.

Where it matters is in your own financial literacy. Understanding that a mortgage is a lien — a legal claim on your property — reinforces why missing payments is serious. It’s not just about damaging your credit. The lender has a documented legal right to take the property back.

Understanding that “home loan” is a broad category helps you shop smarter. You’re not just looking for a mortgage; you’re looking for the right type of loan product for your specific situation, income, military status, or geographic location.

How to Choose the Right Home Loan for You

There’s no universal best answer here — it depends entirely on your situation. But you can narrow it down by asking a few targeted questions:

- What’s your credit score? Below 620, you’re likely looking at FHA or other government-backed options.

- How much do you have for a down payment? Zero down? VA or USDA might be options. Less than 20%? Expect PMI on a conventional loan.

- How long do you plan to stay in the home? Short-term? An ARM might save you money. Long-term? Fixed rate gives you stability.

- Is the home in a rural area? USDA loans might apply.

- Are you a veteran or active-duty service member? Start with VA loans before considering anything else.

- Is the purchase price above conforming loan limits? You’re in jumbo territory.

Talking to at least three different lenders before committing is one of the smartest moves you can make. Rates, fees, and loan products vary more than most buyers realize, and a few hours of comparison shopping can translate into real savings.

Conclusion

The difference between a home loan and a mortgage comes down to scope. A home loan is the broad term for any borrowing arrangement tied to a residential property. A mortgage is the specific legal instrument that secures that loan against your home. In everyday conversation, people treat them as the same thing — and that’s fine. But the more you understand the mechanics behind the terminology, the more confident you’ll feel navigating lenders, comparing offers, and signing documents at closing.

You don’t need to be a financial expert to buy a home. You just need to ask the right questions and understand what you’re agreeing to. That starts with knowing the basics — and now you do.

Frequently Asked Questions

Is a home loan the same as a mortgage?

Not exactly. A home loan refers to the money you borrow to purchase or refinance a home. A mortgage is the legal document that gives the lender a security interest in your property. In everyday use, most people use the terms interchangeably, and that’s generally fine — but technically, they’re two distinct things.

What are the main types of home loans available in the U.S.?

The most common types are conventional loans, FHA loans, VA loans, USDA loans, and jumbo loans. Each has different eligibility requirements, down payment minimums, and rate structures. Home equity loans and HELOCs are also types of home loans, though they’re used to tap existing equity rather than purchase a new property.

What credit score do you need to get a mortgage?

It depends on the loan type. Conventional loans typically require a minimum score of 620. FHA loans can go as low as 580 with a 3.5% down payment (or 500 with 10% down). VA loans don’t set a minimum score federally, but most lenders require at least 580 to 620. A higher credit score generally means a better interest rate, regardless of loan type.